The Covid Panic Brought Even More Economic Zombification

More and more economists and finance specialists are warning of the potential arrival of a new “Minsky moment.” The last time this term was used with such conviction was in 2008 at the onset of the Great Recession. It seems that 2021–22 could have some parallels with the world’s last severe recession.

The Twenty-First Century: The Century of Debt

Up to now, the twenty-first century could be called the century of debt, and if things continue the way they are, it could well be called the century of the great debt default. At the beginning of the century, the extremely low interest rates promoted by central banks in practically the entire developed world caused a frenzy of private credit creation and a gigantic financial and real estate bubble that exploded in 2008 with dire consequences for the world economy.

Central banks, heavily pressured by politicians, redoubled their commitment to low interest rates, causing public overindebtedness to a degree unprecedented in times of peace. In 2020, when the growth model based on the accumulation of public debt and low interest rates seemed to start to weaken, the COVID-19 recession arrived. The worldwide excess of public spending in 2020 has not been corrected, and it does not appear it will be corrected any time soon. The new public debt is adding fuel to the fire. And the accumulation of it (and also private debt, especially that issued by companies) could be reaching the point of no return.

Global debt reached $200 trillion at the beginning of 2011, while global [gross domestic product] GDP was $74 trillion (275 percent debt/GDP). In the second quarter of 2021, global debt reached almost $300 trillion with GDP of $83.9 trillion (330 percent debt/GDP).

Figure 1: Global debt and global GDP

{kind=link}

What Is a Minsky Moment?

Hyman Minsky was a post-Keynesian economist who developed a very insightful taxonomy of financial relationships. According to him, the finances of a capitalist economy can be summarized in terms of exchanges of present money for future money.1 The relationship proposed by Minsky is as follows:

Present money is invested in companies that will generate money in the future.When companies make a profit, they return the money to investors from their profits.Income or profit expectations determine the following:

The flow of present money to companiesThe price of financial assets such as bonds and stocks (financial assets that articulate the exchange of present money for future money)Present business income, meanwhile, determines the following:

Whether expectations about past income (included in already-issued financial assets) have been metHow to modify expectations about future income (and therefore, indirectly, the flow of present money to companies and the price of financial assets issued in the present)Minsky articulates three possible types of income-debt relationship in companies (although he extends the analysis to all economic agents):

Hedge. Hedge finance companies can meet all of their debt obligations with their cash flows. That is, their inflows exceed their outflows. Such companies are stable.Speculative. Speculative companies can pay the interest on their debt but cannot pay down the principal. They are forced to constantly refinance. These companies are unstable, as any minor problem can bankrupt them.Ponzi. Ponzi companies do not generate enough income to pay down the principal or pay the interest. They must sell assets or issue debt just to pay the previous interest on their debt. They end up defaulting on the new debt sooner or later. Their chances of survival are minimal.According to Minsky, when things are going well in an economy and income expectations are met, corporations begin to err on the side of optimism and excessively increase their debt. This causes a shift from a stable situation (in which hedge companies are the norm) to an unstable one (in which Ponzi companies are the norm). In a Ponzi situation, the economy will experience widespread defaults and a financial and economic crisis.

An economy is said to be in a Minsky moment if debtors are unable to pay down their debts (a speculative situation) or unable to pay the interest and the principal (a Ponzi situation).

Minsky was partly right. He accounts for a common truth of financial crises: issuance of debt was abused in previous periods. As a caveat, though, taking into account monetary and financial state interventions—mainly but not solely those of central banks—perhaps the cause of this degradation of debt quality is not a market problem, or at least not exclusively. The crisis may be exogenous to the market (caused by public authorities) or endogenous but amplified by exogenous factors (public authorities contribute to it).

The Economy Has Been Zombifying for Two Decades

As already discussed, global debt has grown more rapidly than the global economy over the last ten years, so it seems credit quality has indeed degraded. The income needed to pay off debt is growing much more slowly than the debt itself.

An additional piece of evidence to support this argument is the increase in the number of “zombie companies.” A zombie company is one whose earnings before interest and taxes are less than or equal to its debt service (it coincides exactly with Minsky’s definition of speculative and Ponzi companies, taken together). A zombie is a wonderful metaphor because a zombie moves and appears to be alive but is in fact dead. A zombie company also moves and appears to be alive—it generates activity, employs workers, and produces goods—but in reality is (almost) dead. It is (almost) certain to die given its inability to pay its debt with its own means. The number of zombie companies has increased exponentially in the United States in recent years, according to a Bank for International Settlements (BIS) report. Furthermore, the probability of remaining in a zombie state has increased. And in fact, zombification is a reality in almost every part of the world.

Figure 2: The rise of corporate zombies

{kind=link}

Source: Banerjee & Hofmann. Note: The various layers of financial intermediation hide this underlying relationship as if it were behind a veil.

Figure 3: Zombie shares by country

{kind=link}

Source: Banerjee & Hofmann. Note: The BIS definition of a zombie company is even more restrictive than ours. It requires, in addition to having an interest coverage ratio lower than 1, a Tobin’s Q lower than the average for two consecutive years (meaning the market values these companies lower than their competition).

However, the BIS data end in 2017. What has COVID-19’s impact been on an already-zombified global economy?

COVID-19 Hit a Zombie Economy: Now What?

The most recent data on company interest coverage (financing cost to earnings) are from the Fed and refer to the North American economy. In the figure below we can see that the median coverage ratio began to fall at the end of 2018, which is consistent with our hypothesis that the economy’s growth model, based on cheap debt, was beginning to run its course. The pandemic has hammered the median coverage ratio. Although the ratio has been recovering since the second half of 2020, it is currently at the level seen in 2009, in the middle of the Great Recession.

{kind=link}

Even more revealing is the interest coverage ratio of the companies in the first quartile (that is, the 25 percent of companies with the lowest ratio). This indicator has been below 1 since 2012; in other words, zombification has accelerated since then. Keep in mind that a ratio lower than 1 means that a company’s profits are insufficient for it to pay its financing costs (it is a Ponzi company).

The interest coverage ratio for companies in the twenty-fifth percentile reached almost 0 just before the pandemic (their profits had almost disappeared). Since then, the ratio has been negative (these companies recorded losses). Observe that these companies have not recovered, while companies in other quartiles have. Their ratio is currently just above −1, which means that their losses (before interest) are nearly equal to their financing cost. This is a total disaster. At least 25 percent of US companies are financially dead.

Valuation of Zombified Companies

One would expect that these companies would begin to go bankrupt, and this is indeed what is happening. According to the Fed, 2.5 times more zombie companies (as a fraction of all companies) went bankrupt in 2020 than in 2019 (

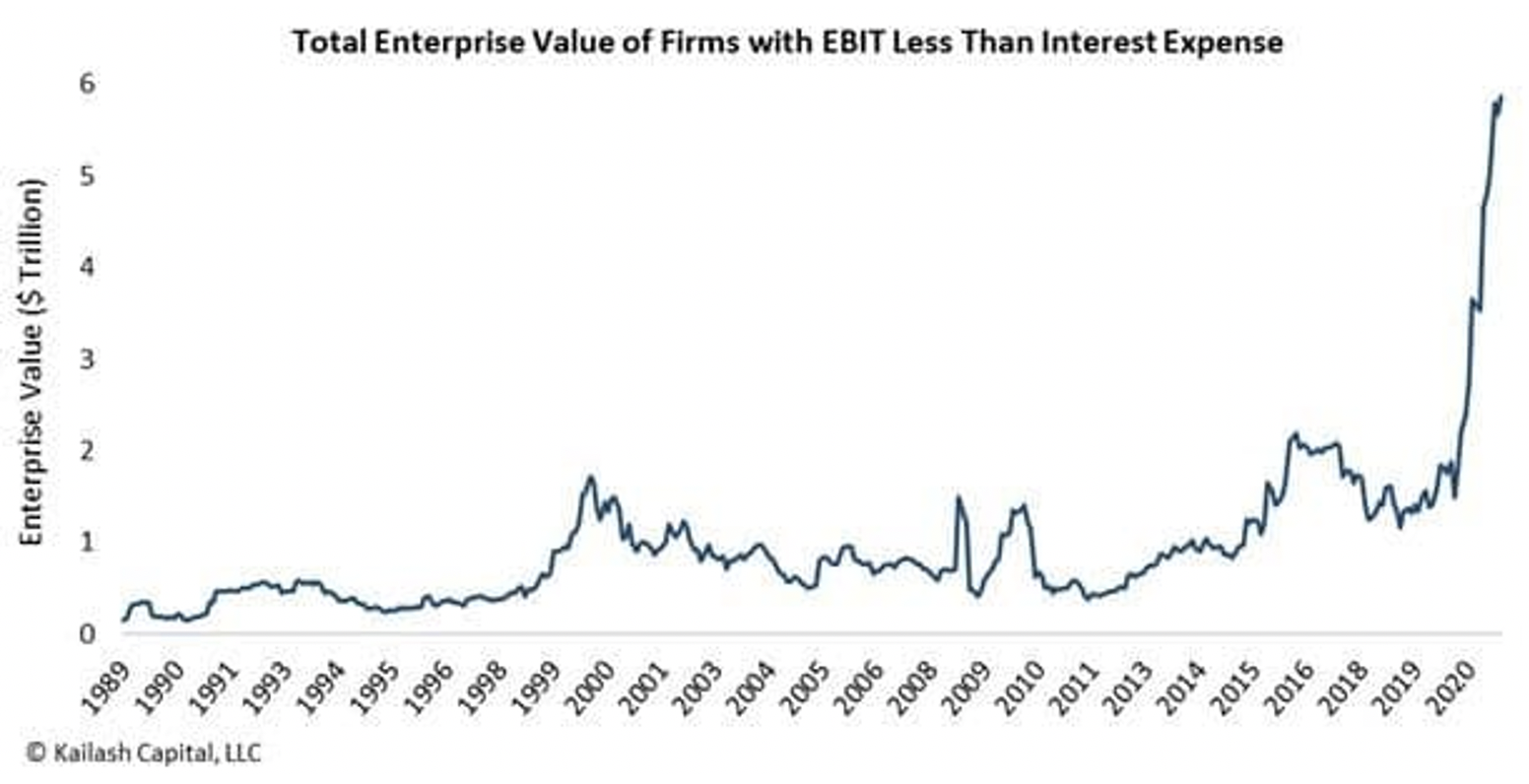

Curiously, the zombie companies that survived 2020 are seeing their valuation skyrocket. Their aggregate value already exceeds $6 trillion, while in 2019 it was close to $2 trillion.2

Figure 5: Total enterprise value with [earnings before interest and taxes] EBIT less than interest expense

{kind=link}

Conclusion

Markets are now extremely complacent. The fundamentals do not seem to justify their optimism. Zombie companies, which were already a problem in 2019, have not only not been killed off but have multiplied. The zombie apocalypse could be closer than we imagine, and we do not have enough Will Smiths in the world to save us.

In a future article, we will analyze the impact of restrictive monetary policy (tapering) on zombie companies.

Legal notice: the analysis contained in this article is the exclusive work of its author, the assertions made are not necessarily shared nor are they the official position of the Francisco Marroquín University.

Originally published at Universidad Francisco Marroquín’s Market Trends.

1. In our opinion, the main problem with Minsky’s view is that he situates his taxonomy in a very flawed macroeconomic theory (a Keynesian one centering on aggregate demand and aggregate supply). 2. Part of the increase can be explained by a greater number of zombie companies and another part by an increase in each company’s valuation.

At least four killed and ...

Rescuers pulled six crew members alive from the Red Sea after Houthi militants attacked and sank a second ship this week, while the fate of another 15 was

Universities threatened w...

Australian universities may lose funding if they’re not judged to be doing enough to address anti-Jewish hate crimes, according to new measures proposed by the country’s first antisemitism

EU’s von der Leyen surv...

European Commission President Ursula von der Leyen survived a no-confidence vote in the European Parliament on Thursday, brought by mainly far-right lawmakers who alleged she and her team