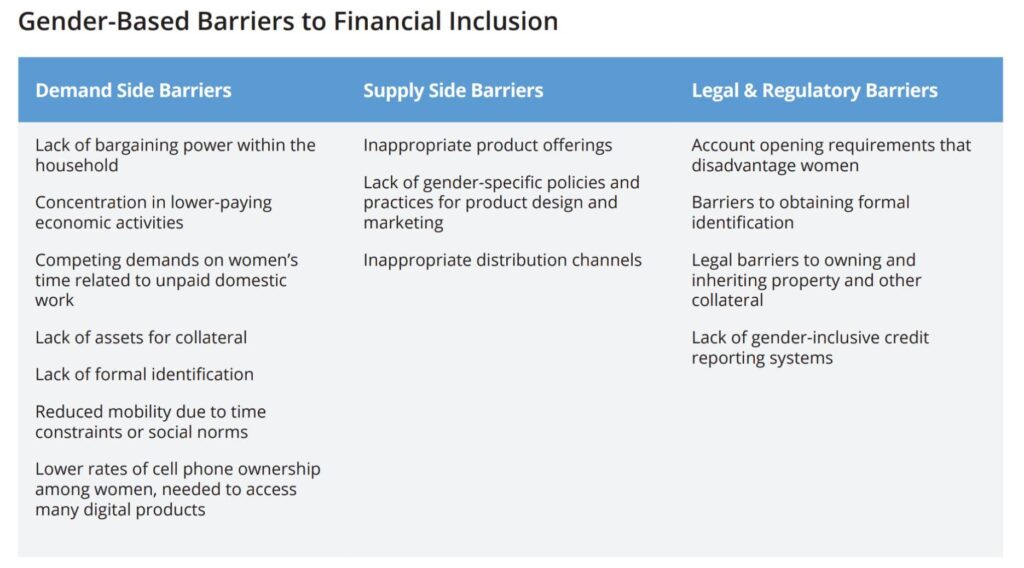

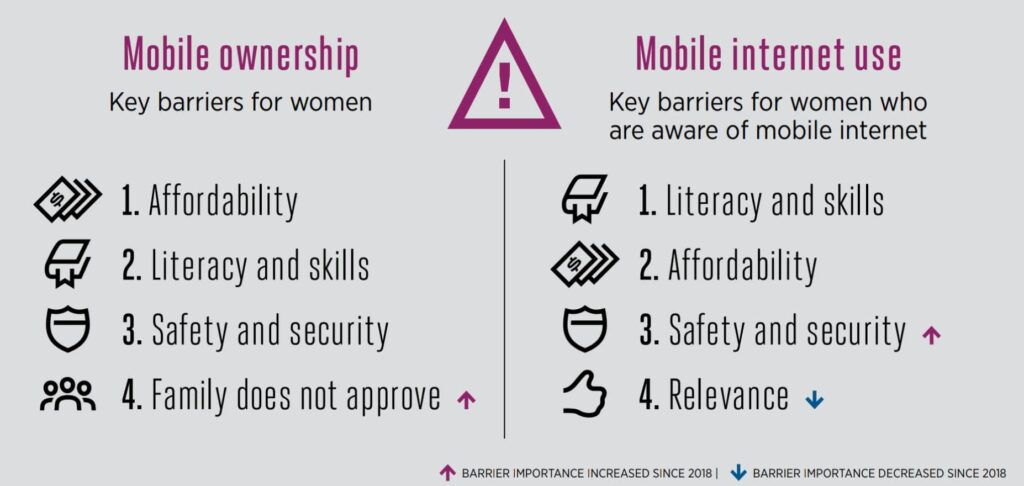

Financial Inclusion: Through a Gendered Lens

The post Financial Inclusion: Through a Gendered Lens appeared first on The Economic Transcript.

Trump says his ‘prefere...

President Donald Trump said Sunday that he would like to “take the oil in Iran” and is considering seizing the export hub of Kharg Island, which is responsible for more than 90% of Iran’s oil exports. Subscribe to read this story

Average U.S. gas price hi...

The average price of a gallon of gasoline hit $4 Tuesday for the first time since mid-2022, as the cost of oil surges due to the Iran war. Subscribe to read this story ad-free Get unlimited access to

The world economy is expe...

Surging oil prices continue to ripple through the global economy because of the war with Iran. Now, some analysts say the worst could still be ahead as the conflict drags on. Subscribe to read this story ad-free