Real Wage Growth Falls for the Twentieth Month as Biden Celebrates Seven-Percent Inflation

The federal government’s Bureau of Labor Statistics released new price inflation data today, and according to the report, price inflation during the month decelerated slightly, coming in at the lowest year-over-year increase in 12 months. According to the BLS, Consumer Price Index (CPI) inflation rose 7.1 percent year over year during November, before seasonal adjustment. That’s the twenty-first month in a row of inflation above the Fed’s arbitrary 2 percent inflation target, and it’s twelve months in a row of price inflation above 7 percent.

Month-over-month inflation rose as well, with the CPI rising 0.1 percent from October to November. Month-over-month growth in price inflation has been positive in 29 of the last 30 months.

November’s growth rate is down from June’s high of 9.1 percent, which was the highest price inflation rate since 1981. But November’s growth rate still keeps price inflation well above growth rates seen in any month during the 1990s, 2000s, or 2010s. November’s increase was the eleventh-largest increase in forty years.

{kind=link}

The ongoing price increases largely reflect price growth in food, energy, transportation, and especially shelter. In other words, the prices of essentials all saw big increases in November over the previous year.

For example, “food at home”—i.e., grocery bills—was up 12.0 percent in November over the previous year. Gasoline continued to be up, rising 10.1 percent year over year, while new vehicles were up 7.2 percent. The only category that showed a year-over year decrease was used cars, which declined by 3.3 percent. This hardly puts used car prices on a path to 2019 prices, however. Used car growth reached 70-year highs throughout much of 2021 increasing year-over-year by over 20 percent or more in every month from April 2021 to April 2022.

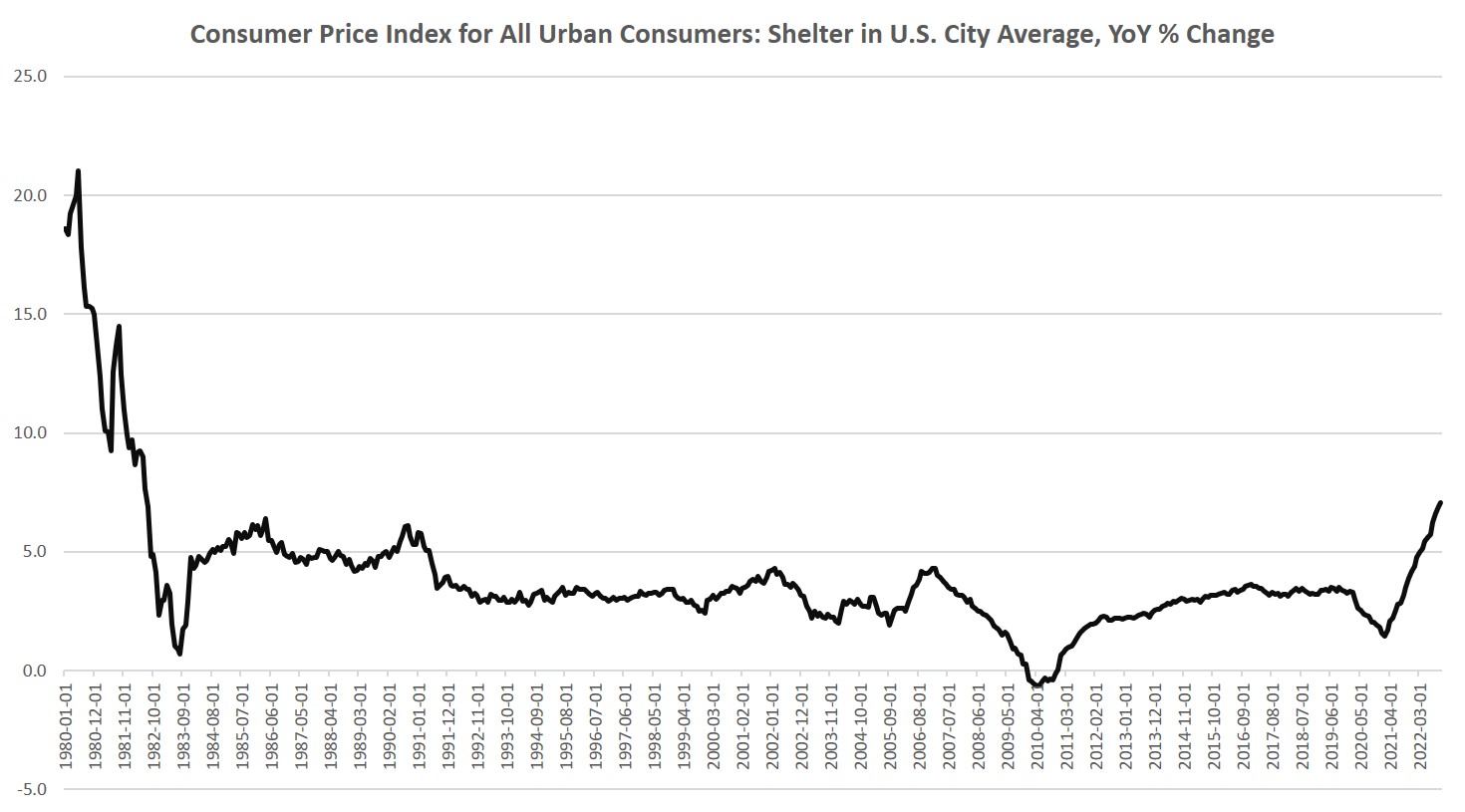

As of November, there is no sign of price growth in shelter slowing down. Last month, shelter prices increased by 7 percent, year over year, which was the highest growth rate since July of 1982. Month-over-month growth in shelter costs also remains among the largest we’ve seen since 1983:

{kind=link}

Meanwhile, so-called “core inflation”—CPI growth minus food and energy—has barely fallen from the 40-year high reached in September. In November, year-over-year growth in core inflation was 6.0 percent. That’s down slightly from October’s growth rate of 6.3 percent. September’s year-over-year increase of 6.7 percent was the largest recorded since August 1982. Month-over-month growth in this measure was positive from October to November as well, with prices minus food and energy growing 0.2 percent. Month-to-month growth has been positive in every month since May 2020.

{kind=link}

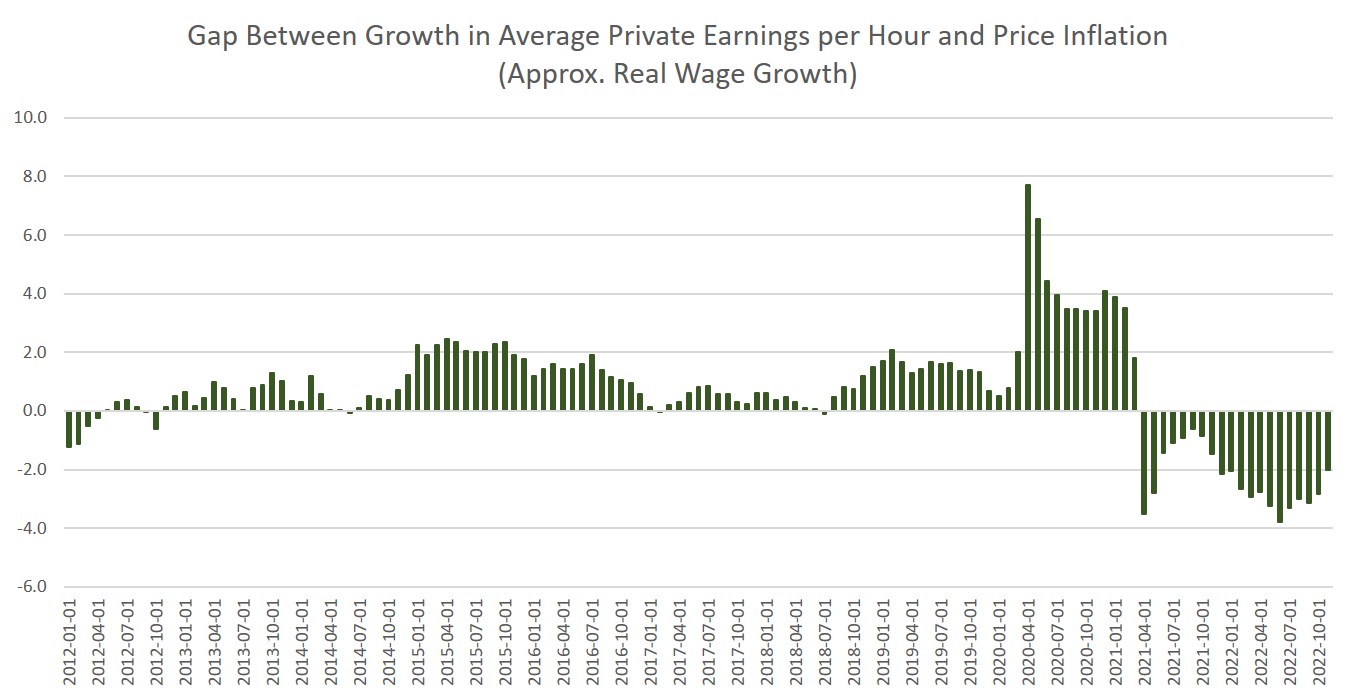

Meanwhile, November was yet another month of declining real wages, and was the twentieth month in a row during which growth in average hourly earnings failed to keep up with CPI inflation. According to new employment data released last week by the BLS, hourly earnings had increased 5.09 percent in November year, over year, meaning wage growth fell behind inflation:

{kind=link}

Celebrate a 7% Inflation Rate?

The Biden Administration today—which has long been rather free-and-easy with how it slices and dices inflation numbers to make itself look better—said inflation is “coming down.” Biden framed it like this:

We learned last month that the inflation rate came down, down more than experts expected…In a world where inflation is rising in double digits in many major economies around the world, inflation is coming down in America.

This is a rather tortured description of the situation. With the CPI rising both month-over-month and year-over-year, it’s a bit of a stretch to say price inflation “came down” in November. It would be more accurate to say the rate of increase “slowed.” Moreover, it’s especially odd to “celebrate”—as CNBC put it—an inflation report that still has price inflation growth over 7%—especially when real wages are falling.

Nonetheless, both the S&P 500 and the Dow Jones ended the day (slightly) up. Given that so much of the market is now heavily dependent on easy money from the Fed, it’s likely that many investors interpreted the slowing inflation growth as a welcome sign that the Federal Reserve might soon bring to an end interest-rate hikes and quantitative tightening. If price inflation is seen to be slowing, this could be interpreted as an excuse for the Fed to force interest rates back down and resume asset purchases.

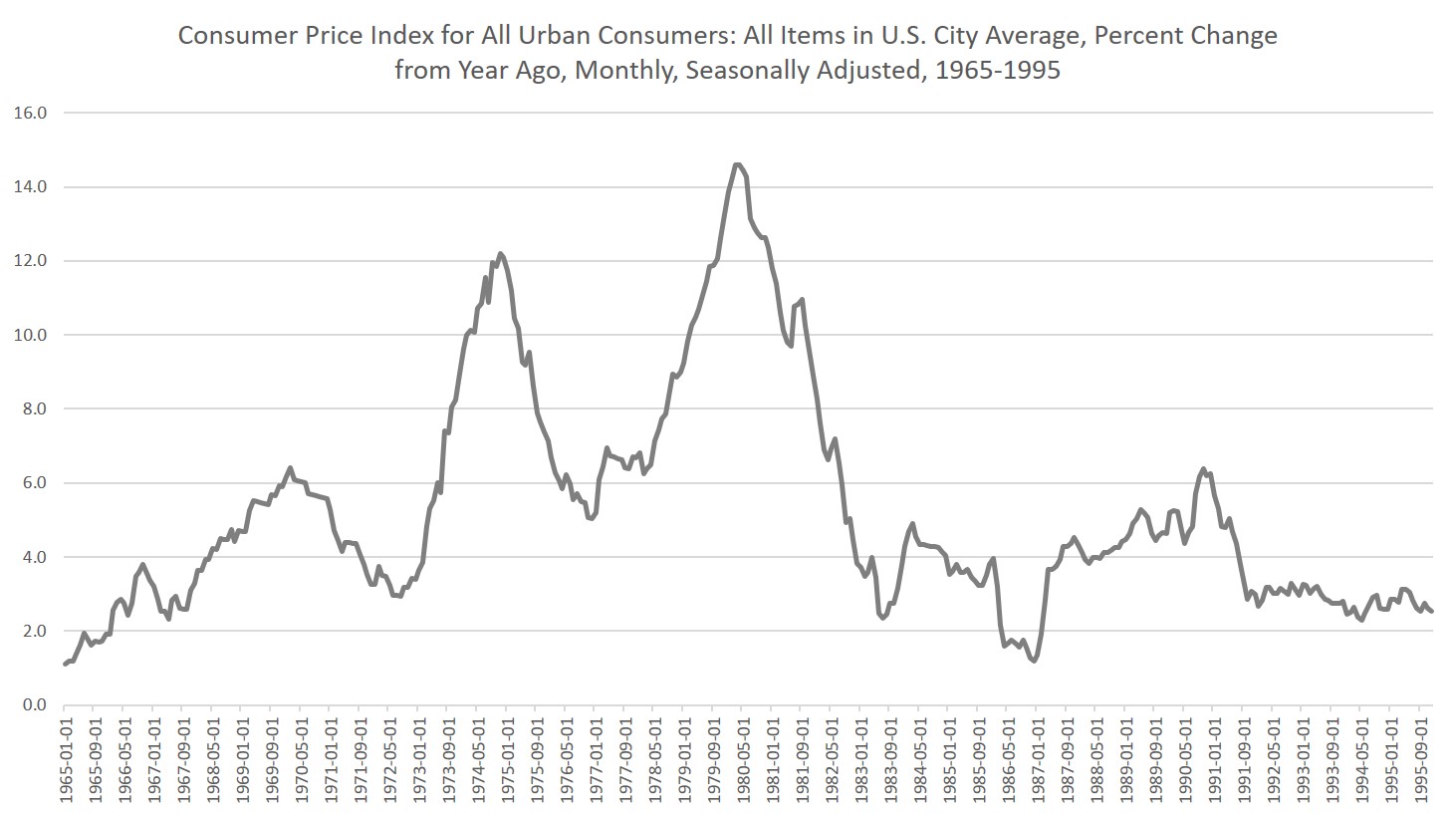

It’s unclear if Fed chairman Fed Powell shares many investors’ rosy outlook however. Powell has repeatedly stated that he fears reversing course on rate hikes lest a return to monetary easing simply set off a new inflationary cycle. In other words, Powell apparently fears becoming another Arthur Burns. The effects of Burns’s failed attempts at reining in price inflation in the 1970s can be seen in the fact price inflation repeatedly ratcheted up during the 1970s in spite of repeated episodes of tightening. BAt that time, price inflation first peaked at 6.4 percent in 1970, then at 12.1 percent in 1974, and then finally at 14.4 percent in 1980 before finally falling in the face of a target policy interest rate at 20 percent. With a current policy rate today at a mere 4 percent, and with no sustained slowing in price inflation growth yet evident, Powell may still fear doing too little.

{kind=link}

Powell’s actual intentions are unknown—and it’s abundantly clear that Fed economists have no more insight into the future of the economy than any other informed observer. Yet many investors are predicting that the FOMC will slow its hikes to the key policy interest rate this month. Instead of the Fed raising the rate by 75 basis points, as it has repeatedly done since June, many investors are now banking on a 50-basis-point increase followed by a pause to rate hikes altogether next month.

As I noted yesterday, Wall Street would love a return to “normal” in which easy money helps fuel relentless increases in real estate and stock prices. At the same time, as interest payments on the national debt continue to mount, Washington policymakers would also love to see a sizable decline in interest rates. In other words, both groups want to declare the “war against inflation” won and over. This has been the hope for months.

Yet, if price growth is slowing, its not be any special virtue on the part of the Fed. We already know that monetary tightening leads to recession which usually leads to slowing inflation. Recent rate hikes and QT appear to be having the expected effect. With home price growth slowing, total employed workers falling, an inverted yield curve, and credit card debt soaring, there’s good reason to guess that recessionary forces are intensifying. That in itself will bring inflation rates down considerably. Wall Street wants to flatten inflation without a recession, however. That’s the so-called “soft landing.” The odds of that happening are getting smaller every day.

At least four killed and ...

Rescuers pulled six crew members alive from the Red Sea after Houthi militants attacked and sank a second ship this week, while the fate of another 15 was

Universities threatened w...

Australian universities may lose funding if they’re not judged to be doing enough to address anti-Jewish hate crimes, according to new measures proposed by the country’s first antisemitism

EU’s von der Leyen surv...

European Commission President Ursula von der Leyen survived a no-confidence vote in the European Parliament on Thursday, brought by mainly far-right lawmakers who alleged she and her team